Theme : Economy

Paper:GS-3

TABLE OF CONTENT

- Context

- Key Indicators from Financial Stability Report

- What led to Improvements of Banking Prospects?

- What causes Resilience and Stability in Banking System

- Achievements of Banking System

- Systemic Risks to Banks

Context : The Budget 2023-24 has no provisions for capital infusion.This reflects the confidence of the government in the robust position of the Indian banking system.

Key Indicators from Financial Stability Report :

- High aggregate deposits: The Indian banking sector recorded a healthy growth in deposits and advances during FY 2022, with the aggregate deposits of the scheduled commercial banks rising by 11.7% and the aggregate advances increasing by 10.2%.

- Decline in NPAs: The gross non-performing assets (NPA) ratio of all scheduled commercial banks (SCBs) declined from 9.1% in March 2021 to 8.2% in September 2022, driven by a reduction in NPAs of public sector banks (PSBs).

- Adequate capital: The Indian banking sector is well capitalized, with the capital-to-risk-weighted assets ratio (CRAR) of SCBs at 13.3% as of September 2022, higher than the regulatory requirement of 11.5%.

- Credit growth increased: Credit growth of banks remained strong during FY 2022, with the credit growth of SCBs increasing from 8.4% in March 2021 to 10.1% in September 2022.

- Moderate liquidity: RBI liquidity management operations during FY 2022 provided significant liquidity support to the banking system and helped to maintain overall financial stability.

What led to Improvements of Banking Prospects?

- Non-impacted by global recession: The financial system remained resilient to external shocks as the overall capitalization of the banking sector improved and credit growth remained strong.

- Stable Rupee: The Indian rupee (INR) remained largely stable during FY 2022, with the rupee depreciating by 0.8% against the US dollar (USD) during the year.

- Stable equity markets: The Indian equity markets performed well during FY 2022, with the BSE Sensex recording a gain of 24.2% during the year.

- High forex reserves: The foreign exchange reserves of India stood at US$ 574.2 billion as of December 2022, a rise of 13.5% over the level at end-March 2021.

- Healthy credit ratings: International rating agencies like Moody’s Investor Service and Standard & Poor’s global rating have upgraded their outlook for the Indian banking system based on its performance in the last couple of years.

What causes Resilience and Stability in Banking System :

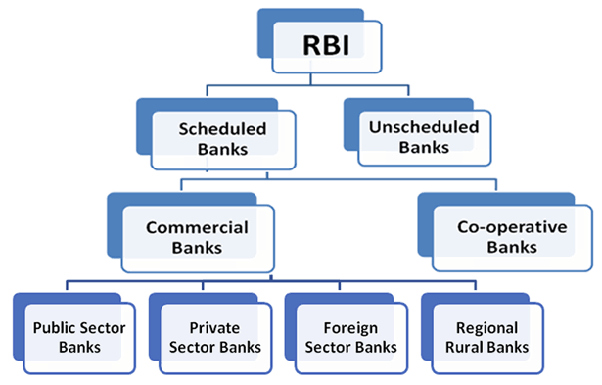

- RBI’s prudency: The RBI as a regulator is excellent and it is well-recognized in the world. It handles the regulation and supervision of such a heterogeneous system involving cooperative banks, foreign banks, and even NBFCs with great efficiency.

- RBI’s global stature: The respect the RBI commands in the world is extremely high. For instance, the Federal Reserve, Washington invited officers of RBI in 2009 after the collapse of the Lehman Brothers.

- Timely assessment: RBI is extremely watchful at the macro, institutional, and individual levels and releases periodical reports like the Financial Stability Report.

- Checks and balances: The Asset Quality Review which RBI initiated in 2018 is crucial in identifying and plugging the loopholes. The banks have deployed a risk assessment department and risk assessment officers. RBI has made various provisions and starts flagging the risks ex. Special Mention Account.

Achievements of Banking System :

- NPA crisis under control: The issues of NPA and Twin Balance Sheet problems were addressed through proactive measures of government and RBI like Recognition, Resolution, Recapitalization, and Reforms.

- Credit Growth: The credit growth in the banking sector has been very impressive in the past few years. The credit to GDP ratio has increased from 48.3% in 2008 to 74.3% in 2018. This has led to increased availability of credit to businesses and individuals.

- Expansion of banking services: The banking sector in India has seen tremendous growth in the past decade. The number of bank branches has grown from around 80,000 in 2000 to more than 1,50,000 in 2018. This has led to an increase in the access of banking services to the masses.

- Financial Inclusion: The banking sector has also played an important role in making financial services accessible to the unbanked population of India. The Pradhan Mantri Jan-Dhan Yojana (PMJDY) launched in 2014 has been a major success, with more than 32 crore accounts opened so far.

- Digitization: The banking sector has seen a rapid digitization, with banks providing various digital services such as mobile banking, internet banking, and cardless cash withdrawals. This has enabled customers to access banking services from anywhere, anytime.

- Financial Innovation: The banking sector has also seen a great deal of financial innovation. Banks have introduced various new products and services such as credit cards, debit cards, and mutual funds. These products have helped customers to access a wide range of financial services.

Systemic Risks to Banks :

- Non-Performing Assets (NPAs): With the rise in NPAs, banks are exposed to the risk of defaults, write-offs and losses.

- Credit Risk: Banks are exposed to credit risk when borrowers are unable or unwilling to repay their loans.

- Interest Rate Risk: Banks are exposed to interest rate risk when their assets and liabilities have different maturities and/or interest rates.

- Regulatory Risk: Banks are subject to stringent regulations and changes in regulations can significantly impact their profitability.

- Operational Risk: Banks are exposed to operational risk from a variety of sources, including technical failures, fraud, and human error.

- Cybersecurity Risks: As banks become increasingly reliant on digital systems and processes, there is an increased risk of cyber-attacks and data breaches.

FAQs :

-

What are Systemic Risks to Banks?

ANS.

- Non-Performing Assets (NPAs): With the rise in NPAs, banks are exposed to the risk of defaults, write-offs and losses.

- Credit Risk: Banks are exposed to credit risk when borrowers are unable or unwilling to repay their loans.

- Interest Rate Risk: Banks are exposed to interest rate risk when their assets and liabilities have different maturities and/or interest rates.

- Regulatory Risk: Banks are subject to stringent regulations and changes in regulations can significantly impact their profitability.

- Operational Risk: Banks are exposed to operational risk from a variety of sources, including technical failures, fraud, and human error.

- Cybersecurity Risks: As banks become increasingly reliant on digital systems and processes, there is an increased risk of cyber-attacks and data breaches.

-

What causes Resilience and Stability in the Banking System?

ANS.

- RBI’s prudency: The RBI as a regulator is excellent and it is well-recognized in the world. It handles the regulation and supervision of such a heterogeneous system involving cooperative banks, foreign banks, and even NBFCs with great efficiency.

- RBI’s global stature: The respect the RBI commands in the world is extremely high. For instance, the Federal Reserve, Washington invited officers of RBI in 2009 after the collapse of the Lehman Brothers.

- Timely assessment: RBI is extremely watchful at the macro, institutional, and individual levels and releases periodical reports like the Financial Stability Report.

- Checks and balances: The Asset Quality Review which RBI initiated in 2018 is crucial in identifying and plugging the loopholes. The banks have deployed a risk assessment department and risk assessment officers. RBI has made various provisions and starts flagging the risks ex. Special Mention Account.